If you own a car and follow the law, there’s a good chance you pay for car insurance.

We all despise it—while secretly praying we never have to use it.

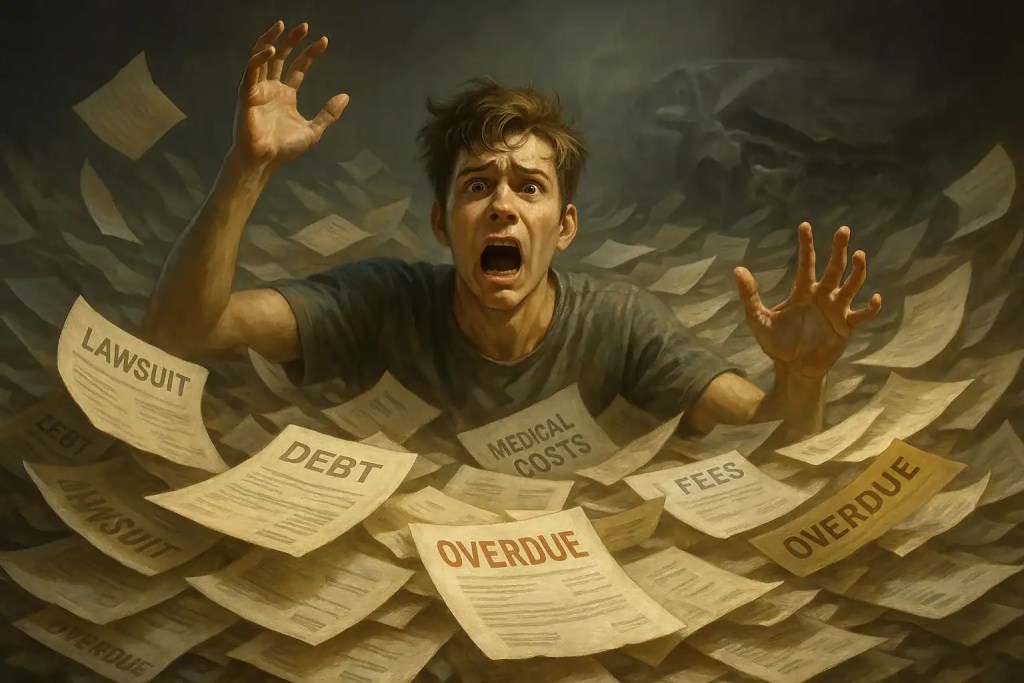

Because if you’re unlucky enough to get into a wreck without it, you’re not just “in trouble.” You’re staring down a mountain of debt so massive you’d start Googling things like:

“How to become a Colombian drug lord with zero experience.”

The Nightmare of Driving Without It

That fender bender you caused while trying to nail the perfect selfie?

Yeah… $5,000 with court fees.

$20,000 for “emotional damage” and $10,000 for “massage therapy” the other driver swears they need—even though they’re out here doing TikTok dances with zero back pain.

Like, “Okay, Becky, we all know you enjoy a good spa day, but you didn’t even get whiplash…”

Regardless, you’re now on the hook for it, pal.

Why We Put Up With It

Or—you could just pay a monthly premium to an insurance company, who will gladly take on that debt for you.

Minus a deductible, of course—because God forbid they actually cover the whole thing.

When you put it like that, car insurance doesn’t seem so bad, does it?

And no, this isn’t Jake from State Farm trying to sell you coverage. This is just me, a guy trying to see the bright side of paying to legally exist on the road.

The Mascot Problem

But let’s be real… some of these mascots make it hard to trust the system.

- Flo from Progressive: Her smile says, “I know where you sleep.” Honestly, she’s got me considering life insurance as an add-on now.

- Geico’s Lizard: Not exactly comforting, though he gets bonus points for sounding like he bartends in Sydney.

- Liberty Mutual’s Emu: If my financial safety net relies on a flightless bird with trust issues, I’m out.

Mascots might be questionable… but at least they have insurance. Which is more than we can say for a scary number of people on the road.

The Scary Truth: Not Everyone Has Insurance

Here’s a terrifying fact: About 1 in 8 drivers in the U.S. is completely uninsured.

So if they T-bone you at a red light? Congrats—you’re now their insurance company.

That’s why uninsured motorist coverage exists… because apparently Dave in his 2002 Honda Civic thought “positive vibes” was a financial safety net.

Why Your Premium Keeps Creeping Up

And just when you think you’re being responsible—safe driving, no accidents, clean record—your premiums still manage to rise every year. Why?

- Uninsured drivers: Remember Dave? Yeah, you’re basically paying for his vibes.

- Medical costs: A Band-Aid costs $400 now. Imagine the bill for real treatment.

- Car repair inflation: Your bumper has more sensors than a NASA rover. That’s not a $200 fix anymore.

- Fraud: People really out here faking back pain for spa weekends, and you’re footing the bill.

Insurance companies aren’t shy about passing those costs onto you—because why should they be?

How to Lower Your Premium (Because Apparently “Being a Good Person” Isn’t Enough)

Is anyone else tired of seeing those fake car insurance ads that scream:

“Living in Utah? Find out how you can pay as little as $50 for car insurance!”

Yeah, if it sounds too good to be true… hate to break it to you, but it probably is. And if it really is $50 a month, you’re probably signing up for a $5,000 deductible plan with zero roadside assistance.

Flat tire? You better know how to change one or you’re stranded.

Dead battery? You might as well start walking.

Good luck, Bob.

“Look, I’m not here to sell you insurance (thank God). But if you’re tired of the gimmicks and actually want to know how to shop smart, Consumer Reports has a legit car insurance buying guide you should read: Consumer Reports Car Insurance Buying Guide.”

If you’re still with me —there actually ARE ways to shave some dollars off your monthly bill without selling a kidney. Here are a few:

- Bundle, Baby – Got a house? Renters insurance? A boat you regret buying? Slap it all under one company. Insurers love bundles more than Starbucks loves inventing new Frappuccino flavors.

- Raise Your Deductible – Translation: “I’ll cover more if I crash, you cover less.” Risky? Yeah. But if you’re not the type to turn left while eating soup in the car, it might save you cash.

- Good Credit = Good Rates – Insurers basically think: “If you’re bad with money, you’re probably bad at driving too.” Rude? Yes. Effective? Also yes.

- Drive Less, Pay Less – If your car spends more time parked than moving (looking at you, Netflix bingers), consider mileage-based insurance.

- Defensive Driving Courses – Take a class, learn how not to tailgate every minivan you see, and get a discount.

- Ask for Discounts – Safe driver? Student? Military? Alien abductee survivor? (Okay, maybe not that last one.) But seriously, companies don’t always tell you what you qualify for—so ask.

- Stop Speeding, Karen – One ticket usually won’t jack your rates up too high, but get more than one within a short time frame and you can kiss that little “good driver” bonus goodbye. Congrats—it’s now funding the expensive premium you just earned yourself.

Car Insurance Myths You Probably Still Believe

Let’s bust a few car insurance myths that refuse to die, kind of like that one uncle who insists “back in my day gas was 25 cents a gallon.”

- “Red cars cost more to insure.”

Nope. Doesn’t matter if you drive a firetruck-red Mustang or a beige minivan that screams “I gave up.” Insurance companies don’t care about your paint job—they care about your driving record, the car’s safety features, and whether you think stop signs are optional. - “Older drivers always pay less.”

Not exactly. Sure, being 40 looks better on paper than being 19 with a TikTok addiction, but premiums can climb again as drivers age into their 70s and beyond. Basically, you’re either too young and reckless, or too old and fragile. Enjoy that sweet spot in the middle while it lasts. - “Full coverage means everything is covered.”

Ah, the biggest scam of all. “Full coverage” sounds like the insurance equivalent of an all-you-can-eat buffet… until you find out it’s more like a sad salad bar. It usually means liability + collision + comprehensive—but it definitely doesn’t mean the company is covering everything. Spoiler: if you drive through a lake because you “thought it was shallow,” they’re not cutting you a check. - “Expensive cars always cost more to insure.”

Mostly true… but not always. Luxury cars are pricier to fix, more likely to be stolen, and cost way more to replace—so yeah, higher premiums. But some expensive vehicles with insane safety features (like Volvos or certain SUVs) can actually be cheaper to insure than a flashy sports car. Translation: the safer and less stealable your ride is, the less you’ll pay—even if it’s worth more.

And hey—next time you knock the dad driving around in a minivan, just remember he’s probably paying WAY less for insurance than you are with your convertible.

Final Thoughts: Hate Paying It, Love Having It

Car insurance is one of those things you hate to pay for, but absolutely love to have when life throws a plot twist at 40 mph.

So, tell me:

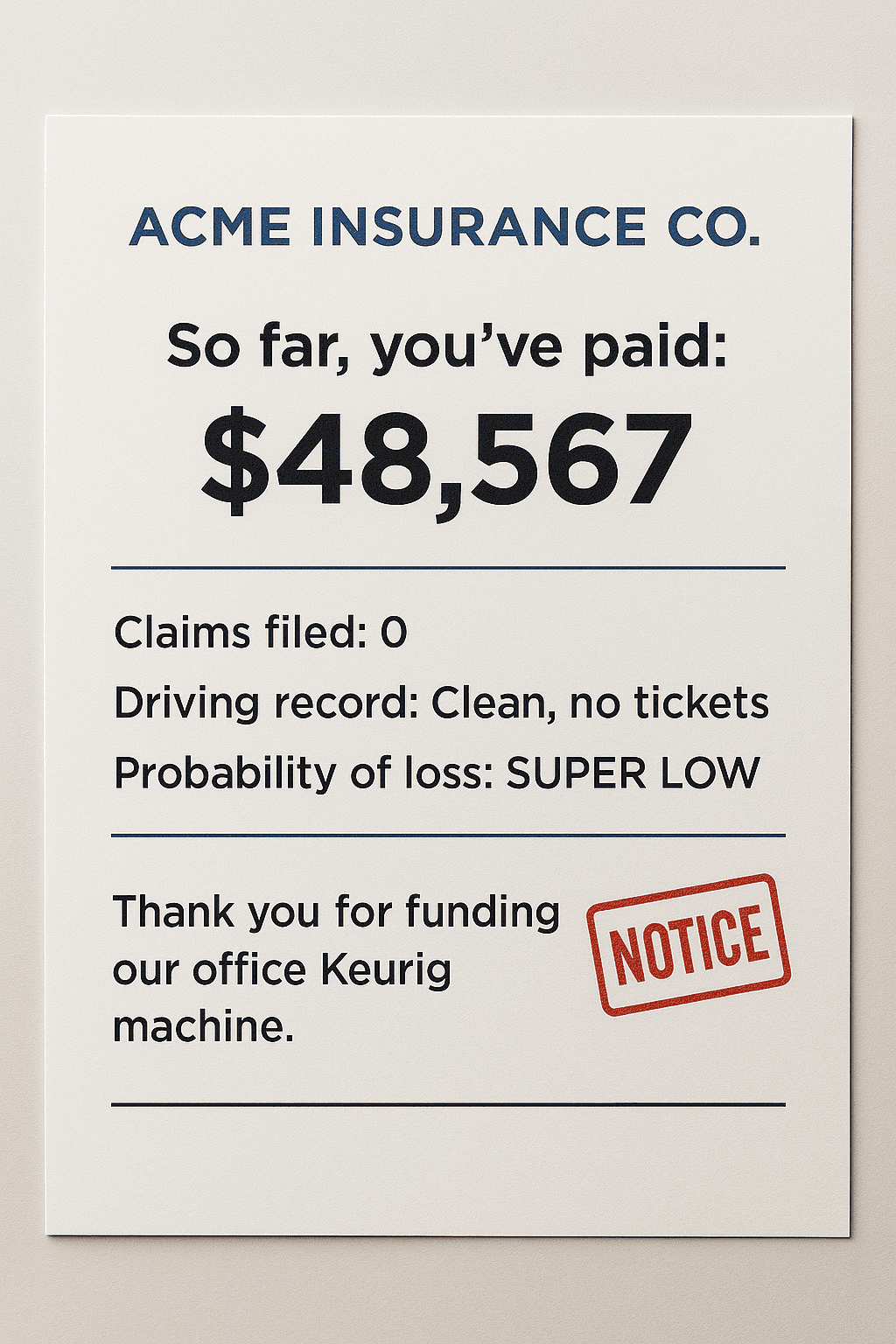

- Should you get a golden plaque at your local insurance office for single-handedly funding their Keurig machine?

- Or are you rolling the dice, hoping your cousin Vinny can fix your bumper for the cost of two pizzas?

I’ve never been the gambling type, so I’m sticking with the $500 deductible plan.

GratiDude out.

Leave a Reply